Welcome to the new Traders Laboratory! Please bear with us as we finish the migration over the next few days. If you find any issues, want to leave feedback, get in touch with us, or offer suggestions please post to the Support forum here.

BlueHorseshoe

-

Content Count

1399 -

Joined

-

Last visited

Posts posted by BlueHorseshoe

-

-

Hi BlueHorseA windows help file is identified by a *.chm extension

Would U mind 2 have a look into your

tradestation\Program\

or make a search with a *.chm filter in your TS main program included subdir ?

If TS 9.1xx dir structure = 8.xx

U should find the help file named something like :

easylanguagehelp.chm

Please rar it B4 attache it

Anyway many ThanX 4 your gently help

aaa

Hi,

I have already checked in the folder you reference (see my previous post) - the only files with .chm extensions are those I listed. Could TS have changed the name? Is there somewhere else I could look?

Kind regards,

BlueHorseshoe

-

Hi everyoneI am wondering if you could help me to detect a flat moving average

Thank you in advance

No idea what you mean (I'm sure that you do though).

Please repost your request giving more information. Use an image if that will help you to explain.

Regards,

BlueHorseshoe

-

Gorgeous curve! Comes with a cold and hard slap of the invisible hand of reality too.What amused me was that I thought I'd would have to keep running the code and eventually it would produce a nice looking curve. But the "gorgeous" curve came on the first pass - then none of a further twenty or so attempts produced anything even halfway decent.

Now what were the chances of that?

Kind regards,

BlueHorseshoe

-

WHY DO YOU USE INDICATORS THAT CHANGE VALUES WHEN PERIOD CHANGES?Dump the word "indicators". It is obscuring the issue.

Your question is:

"Why do you use a comparison of current price to historical price that changes when the historical price upon which the comparison is based is changed?"

Using summation as an example, the answer can be given as follows:

A = B + C ∧ D <> C ⇒ ¬ B + D = A

I hope that helps.

BlueHorseshoe

-

Hi Mitsubishi,

Not sure I like your tone . . .

I like your idea of trading as many instruments as you possibly can at once so you don't lose potential profits by only successfully trading one or two.

The "idea" isn't diversification. It's applying position sizing to individual markets/strategies rather than to a whole portfolio.

If you don't think that idea has merit but you're not prepared to provide concrete reasons for why, then any kind of discussion will be difficult.

It's this kind of mental approach that separates the theorists from the wannabe traders.

I enjoy theory. I spend a lot of time looking at theoretical trading methods around market microstructure that I know I'll never have the capital or technology to do anything with. I'd also like to apply my longer term ideas to trading a large universe of stocks, but I don't have the capital so the costs would kill me. So it's all just theory for me.

I also trade. End of day. Not automated, but entirely rule based. One single approach. It's very boring.

What I have described above is incorporated into what I am doing - past performance in each particular market is a factor in position sizing for me.

Are you planning to start a room soon?

Nope. Just trying to share ideas with other people here for free and hopefully get some feedback from those with more knowledge and experience. Just the usual. Nothing sinister. If people don't find it useful then it's no big deal - it's just a way to pass the time . . .

Kind regards,

BlueHorseshoe

-

Hello, May I ask why you need someone else to acquire this for you? Regards, BlueHorseshoe

Dear BlueHorse

I use MC in PowerLanguage very similar than EasyLanguage in TS.

Scripts compiled after TS 9 are unfortunately no more compatible with MC.

They are new functions and "Method".

Also TS help is much better documented than MC help

( Please, have a look in the attached file Help of the tiny MC help )

and May B It could help coders w/o TS platform 2 have the latest release of EasyLanguage help file ...

Best regards

aaa

PS It's ONLY one help file (*.chm must be compressed 2 upload it ), not the entire program of course !

Hello,

I'd be happy to help, but the only compiled html files I can find in the Program directory are:

elanalysis

elobject

elword

spr_topics

tradestationhelp

tsdevhelp

Any suggestions to help me find what you're looking for?

Kind regards,

BlueHorseshoe

-

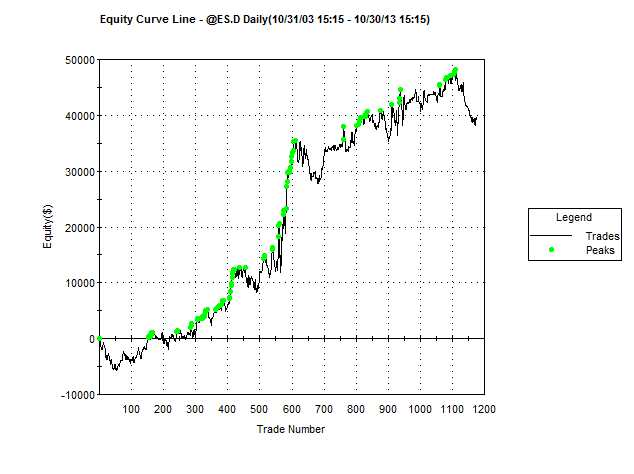

Are you REALLY serious about making SUBSTANTIAL profits trading the financial markets? Then take a look at the equity curve for the AMAZING trading strategy below . . .

- Profitable over 10 years of ES data

- Contains no element of curve fitting or optimised parameters

- Sample size of well over 1000 trades

Wouldn't you love to be able to trade with this FANTASTIC strategy that just keeps on WINNING? Imagine what these PROFITS would look like if you traded more than one contract or many markets at once!

ONE-TIME SPECIAL OFFER - NUMBERS STRICTLY LIMITED - GET THE STRATEGY AT A 20% DISCOUNTED PRICE OF JUST $3800 !!!

BlueHorseshoe

// Buys or Sells Short randomly on Mondays, Wednesdays, and Fridays // One day holding period // Generated attached equity curve on first attempt if Dayofweek(date)=1 or Dayofweek(date)=3 or Dayofweek(date)=5 then begin if random(10)>4 then buy this bar else sellshort this bar; end; If Barssinceentry=1 then Setexitonclose;

- Profitable over 10 years of ES data

-

HelloCould someone post here his last TradeStation release 9.1.24 "easylanguagehelp.chm" file located in the program dir ?

https://www.tradestation.com/trading-technology/whats-new/tradestation-9-1

Hello,

May I ask why you need someone else to acquire this for you?

Regards,

BlueHorseshoe

-

Here is another experiment:

The BH is a contract that is very similar to the ES. It exhibits the same volatility and the contract value is identical. When BH moves 1 point, you stand to make or lose $50, just as with the ES.

You have a strategy which you may trade in either or both of these contracts.

You also know the historical performance of the strategy in each of these markets:

BH 20%

ES (20%)

What do you do?

Fast forward 1 year, and the returns for each market are now as follows . . .

BH (20%)

ES 20%

The trader who decided to only trade the BH, where historically the strategy had been profitable, has lost 20%.

The trader who decided to trade single contracts in both the ES and the BH has broken even.

The trader who decided to trade both the ES and the BH applying a fixed fractional money management approach is (roughly) breakeven. Though the profits from the ES would have allowed larger position sizing, this would have been reflected in the position sizing for both markets, so the losses in BH would also have been correspondingly larger.

The trader who began trading single contracts in each market but increased position-size for each particular market based on the strategy's profitability in that particular market should show a net profit. His single contract returns for ES would be negated by his single contract returns for BH, but he would have been trading multiple contracts of ES, leaving a net profit.

I have described what is hopefully a worst-case scenario again here; if you think you have a great strategy, then maybe it would have made 50% in one market and only lost 2% in the other, or whatever . . .

The outcome for a strategy isn't based on all of the price change of the instrument it is applied to - all that matters is the price change at those times when strategy and price intersect (when you have a position) - call that limited set of prices Data Set A. If a second strategy intersects with different prices and we call these prices Data Set B, then when you compare Data Set A and Data Set B you will have two different sets of price, which is pretty much the same thing as having two different markets. Hence exactly what I have described above with the ES and BH could be applied with two different strategies in just one single market.

BlueHorseshoe

-

Far be it from me to disrupt this potentially excellent thread bud (as yet to manifest it's own humble ambushions)

I wouldn't worry about that - I'm surprised the thread ever re-surfaced!

Whether price is random or not doesn't really have too much to do with the original point I was trying to make - assuming that it is (I don't) is just the easiest way to present the concept and removes the possibility of any objection on the basis of a trader's inability to predict prices (which, ironically, is the argument you're now trying make in reverse!).

The thread is posted under "Money Management" because that is what it is about.

I would summarise its main points as follows:

- Rather than applying a position-sizing formula to a portfolio based on the net profitability of that portfolio, it may make sense to apply the position-sizing to each strategy or market individually, based on the net profitability of that strategy or market.

- This can include situations where the strategies are applied in the same market, and even those where they are applied simultaneously so that, in single contract terms, they are completely neutral (pre costs).

I'm far more interested to hear reasons why this money-management approach is flawed than I am in discussions about whether price movement is random.

BlueHorseshoe

- Rather than applying a position-sizing formula to a portfolio based on the net profitability of that portfolio, it may make sense to apply the position-sizing to each strategy or market individually, based on the net profitability of that strategy or market.

-

This is not random................................Assume the crowd are just a bunch of random people in a shopping centre (or "mall", for most of you) . . . I would be willing to bet that the next person to walk up to that karaoke machine was a worse singer.

That's random.

That's regression to the mean.

BlueHorseshoe

-

Player B for me

OMG my message is too short so I had to write this :crap:

Obviously.

Now consider another game. A market will either tick up or down with each trade. If there are five consecutive up ticks or down ticks, Player A wins £200. If there are not five consecutive upticks or downticks, then Player B will receive £20.

Who would you sooner be, Player A, or Player B?

BlueHorseshoe

-

I personally do believe markets are not moving randomly otherwise consistant profits could not be made......even if only a pattern is becoming repetitive and the rest is random, still means the "randomness" label can't be applied there.TW

Hi TW,

I agree with you - I don't think markets are random either, not all the time, but . . . if they were I think they would be far easier to trade, not more difficult. It is natural to associate "random" with "unpredictable", but this is a mistake.

Random price movements conform to predictable distribution models.

Consider the following game:

I will toss an evenly weighted coin multiple times. If there are five heads in a row, Player A receives £200. If there are not five heads in a row, Player B will receive £20.

Who would you sooner be, Player A or B?

I look forward to your response . . .

BlueHorseshoe

-

Hi,Edit: Right, so i think ive answered my own question through research. The reason for the capital requirement is the "initial margin" requirements set by the exchange CME+broker. As far as i understand it they require around $4500 as a form of liquidity(insurance) per contract, pretty much to do risk management for you..? Still seems high to me given the actual movements a contract typically can do.

--

I'm a noob. And i keep reading about how E-minis require relatively huge capital to trade safely, but dont understand it. I've also noticed all the warnings of it being extremely risky for those who do not understand it, hence this post.

So the advice i keep seeing is to have a bankroll of $5000-$10.000 PER contract you trade.

A general observation of the ES is that it tends to move 15-30 points an average day. It is also very rare to see it move more than 10 points in 1 hour, usually averaging 2-4 points of movement an hour.

In contrast to forex, this seems a lot "safer" - making the likelyhood of huge sudden moves a lot lower.

Now, not that any strategy would allow this to happen, but lets take a worst case scenario. You've got $5000 on your account, and buy 1 ES contract when it opens. You for some reason ride the downtrend and the ES closes 30 points down. Netting you a loss of 30x$50 = $1500. You still have $3500 left.

Now, if you have a long term strategy that must allow for huge stop losses, then i can get behind the $5000 recommendation. However, if i were to guess, i would imagine most strategies(at least mine would) use a SL of.... 2-5 points? $100-250 potential loss.

Then my question is, why would you advise having a $5000-10.000 bankroll, when your worst case SL stops you out at a $100-250 loss?

Is this the "max 2% capital risk" rule in action?

Dont want to come off seeming reckless here, but somehow this just seems a bit overly cautious to me?

Appreciate any thoughts!

Hi Daniel,

I think there are two elements to your thinking here, and you need to be careful not to confuse them.

1) The notion that a margin of $4500 is actually a rational requirement is probably nonsense, as you suggest. In as much as it is to provide liquidity insurance, the ES is incredibly liquid and it is hard to imagine (even in a flash-crash type scenario) that a broker would decide to liquidate a position you had and then find that the market had to move 90 points before they could do so. The ES probably goes lock limit before then (you can find the exact details on the CME website), however, and in that situation your broker becomes just as stuck as you, so . . .

2) None of this really has anything to do with the size of your account or how much you should or shouldn't risk on each trade. Margin - you've said it yourself - is liquidity insurance for a leveraged product, and that is not the same as the money management approach you take when trading.

I imagine another reason that the broker has the margin requirement is that they prefer to have that money in their account rather than yours.

Kind regards,

BlueHorseshoe

-

This is an interetsing conversation. I haven't read all 9-10 pages of this thread yet, but had a few thoughts.First, I think that scalping is alive and well and has just morphed into being done by HFT computers instead of locals in the pits. It used to be the locals could get better fills and were in-and-out with a few ticks before we could call-in to our broker, have him call the pit, place our orders and get confirmation numbers. Even if you did a lot of volume and had a dedicated phone line you were still slower that the locals. When markets went electronic, everyone effectively had the same shorter-time advantage and pit scalpers died out. Now electronic traders have to give way to HFT computer scalpers . . . who give way to those with faster computers . . . who give way to those with faster computers closer to the Exchange, etc.

Second, "scalping" is a relative term. Going for 1-2 ticks is scalping but so too is going for 5-10 ticks in a fast market like CL (Crude Oil) or GC (Gold). All I've done is raise my level of scalping above the noise generated by the HFT computers' whip in those markets. I can't compete with the HFT computers for 1-2 ticks, or even 5-10, but can take out 10-15 -- which I still believe is scalping.

But I disagree that the CME is still FIFO. At least without question. That's what was said for a long time before the existence of dark pools became known -- whereby HFT computers were allowed (for a price the Exchange didn't want to talk about) to "jump" the queue and get filled ahead of a limit order that had been sitting there a lot longer waiting for its fill.

I've traded CL for years and have a system to pick turning points in advance (sometimes). I've had my limit orders sitting there and can see the DOM as it comes into them and there is a total of, say, 5 at my level. Part of that is me. Price has way too often come into that level, hit it exactly and turned and I didn't get filled. I know I should have been #1 or #2 in the queue and can only guess I was "jumped" by a HFT computer. I can't prove it though.

Good Luck!

Chartsky

NYMEX / CME certainly claim that the CL contract is FIFO:

BlueHorseshoe

-

Using the Easy Language Collections Global Dictionary it is quite easy to store any value from any chart and then retrieve and plot that value on any other chart from any other time frame.Once calculated code like this posts to the global dictionary with a time based key that is down to 1 second granularity.

Thanks - I didn't know how to do any of that (although I was aware it could be done) - it may be useful to me in another context.

Always good to see you back on the forum!

Kind regards,

BlueHorseshoe

-

How do I combine different time frame chart indicators? I am using Tradestation and trade the e min. I am trying to add the @es 60 minute chart Floor trader pivot levels indicator on a 1500 tick bar chart.Thanks for any suggestions.

Chris Tina

Hello,

This is pretty tricky to do. Not impossible, by any means, but probably more hassle than it's worth . . .

Before spending any time trying to help you do this, I'd like to try and help you in another way:

"Floor Trader Pivots" are just averages. They take a few data points as inputs, and then calculate a rather convoluted weighted average of them. There is absolutely no reason whatsoever to imagine that there is anything special about the price levels they produce. No reason to expect such levels to act as support/resistance, or that price will "breakout" from them.

In short, I think that they're a complete waste of anyone's time. I spent a reasonable amount of time looking for strategies around these levels, and could find absolutely no edge whatsoever, even with a ridiculous amount of curve-fitting in the strategies.

I could be completely wrong, of course, but my advice would be to look for a different way to trade. If you're desperate to continue with 60min pivots on tick charts, then say so and I will try and find a simple way to help you do this.

Kind regards,

BlueHorseshoe

-

It's always fun to read about the misfortunes of other:

BlueHorseshoe

-

Here is one reason why HFT has made scalping harder:Note that scalpers use limit orders (except on stops). Here are 2 situations:

1. assume a scalper has a bid in at 1434 waiting for a retracement. His bid will be sitting behind a large number of HFT orders. If 1434 is a price of strong support, all the HFT orders must be hit before his order is. If he does get hit, and puts in his sell at 1435, his order again will be behind all the HFT orders, again making it less likely that he will get hit than before the "HFT era."

2. assume, instead, that the market is moving down and 1434 is no longer a place of support. (The algos will determine this in a very small fraction of a second). As soon as the first market sell at 1434 is made, all the HFT bid orders will disappear, and the scalper will be immediately filled in a declining market.

Result: Fills are worse now than in the pre-HFT era. Therefore: the more important getting good fills is, the less likely success with the trading method has become. For swing trading small orders, the difference is very small. For scalping ticks, it is quite significant.

As was discussed in the earliest pages of this thread, this is all debateable and depends on the instrument in question.

For instance, most CME futures order books are FIFO, so there is no mechanism whereby HFTs can guarantee that they are ahead of you in the queue - they can't queue jump.

Secondly, there are restrictions on fill-to-cancellation ratios, and fines if a trader or HFT overshoots them (not an issue to pay the fines if you're trading massive size and making a lot of money - they're just another predictable fixed cost, I guess).

Then there is the point that as soon as market orders start to cross the spread hit the bid the HFT can tell whether the market will continue to decline (pulls it's orders) or whether the level will hold and a profit can be made . . . If it can do this (directional prediction) then why is the speed/limit order advantage even required?

Finally, supposing that the HFT "thinks" the level will hold as support and a profit can be had - it then decides to put a limit order into the orderbook somewhere overhead in order to take profit - it can only join the back of the queue when it does so, behind all the other orders already resting at that price.

I think the general gist of what you're saying is correct, but when it comes to the details and mechanics of what's going on, none of us really know . . .

BlueHorseshoe

-

I would like to find the voodoo lines, any help with this?I think Baron Samedi might have them . . .

BlueHorseshoe

-

Ok, i got it. One has to enable multiple Positions in the same direction in the strategy properties...

Hi,

Yes, you do indeed - one of those little TS quirks!

You would do well to spend some time exploring all the aspects of the strategy properties box, especially those relating to the way in which the software simulates order fills.

Regards,

BlueHorseshoe

-

Poisonous Oats is quite plausible and already affects people today. Well maybe not poisonous, but for those people they may as well treat it as poison because the effects can be lethal if prolonged. Those people are celiacs.Are you certain? Are Oats and Wheat the same?

Actually, forget that - we don't want to derail the thread with a discussion about cereals . . .

BlueHorseshoe

-

You can use place orders in SIM, but only for instruments of the same type as the account. In other words, if you have a TS Forex account, you can't live SIM trade a futures contract. This is because the data-feed is not live, and you're getting delayed data. There is no way around this (TS will not allow you a live Futures feed to a Forex or Securities account, as far as I am aware).

Does this sound applicable?

Regards,

BlueHorseshoe

-

I think you already have your answer above, don't you?

Not sure why you even need an automated strategy for this though - why not just place a resting order at the price level you want, as it sounds like you're going to be around to watch the whole process unfold?

BlueHorseshoe

Official Launch of My Crude Oil Trading Room This Monday Nov. 4th

in Futures

Posted

Looking at the chart he's posted, my guess is that it's the other way around - he perceived it to be support because previously it was resistance. Until it wasn't. And isn't.

Hmm . . .

Even if you think of support as an area where participants have rejected lower prices, the questions remain - who are those participants, did they actively buy when they wouldn't buy at higher prices, or was there a dearth of passive sellers at lower prices, do they still hold positions established at those prices, and how will they react if price trades back down to them?

When I think of "support" I think of a massive buy-side institution with a 3 year outlook that will simply shrug and chuckle at a retest of that price, or an algorithm that is long since flat because they turned off and went home for the night.

If you can know (or guess with some certainty) who these participants are, their goals and limitations, then support becomes a workable concept.

BlueHorseshoe