Welcome to the new Traders Laboratory! Please bear with us as we finish the migration over the next few days. If you find any issues, want to leave feedback, get in touch with us, or offer suggestions please post to the Support forum here.

Garylim

-

Content Count

24 -

Joined

-

Last visited

Posts posted by Garylim

-

-

I assume CQG doesnt have the code again? or is it under a different study name?

-

Here is the full curves for CQG. Could any1 please take a look to see if anything is missing?

I noted that the std deviation are all constant from each other so there is something wrong but i do not know what.

HELP !!!

Deviation 3 Curve:

day:= BarsSince(BarIx(@,StartOf Day) = 0,1,10000)+1;

day2:= BarsSince(BarIx(@,StartOf Session) = 0,1,10000)+1;

priceX:= IF(price = 1, Close(@), IF(price = 2, High(@), IF(price = 3, Low(@), IF(price = 4, Mid(@), IF(price = 5, HLC3(@), IF(price = 6, Avg(@), IF(price=7, Open(@), 0) ) ) ) ) ) ) ;

vol:= IF( HasVal(Vol(@)) AND Vol(@) > 0, Vol(@), 1) ;

a:= Sum(priceX* vol,day)/ Sum(vol,day);

b:= Sum(priceX* vol,day2)/ Sum(vol,day2);

c1:= Sum(priceX* vol,Period)/ Sum(vol,Period);

VWAP:= IF(DaySessionPeriod = 1, a, IF(DaySessionPeriod = 2, b, IF(DaySessionPeriod = 0, c1, a) ) );

DAYSES:= STDDEV(@,day)/100;

SES:= STDDEV(@,day2)/100;

ANY:= STDDEV(@,Period);

STD:=IF(DaySessionPeriod = 1, DAYSES, IF(DaySessionPeriod = 2, SES, IF(DaySessionPeriod = 0, ANY, ANY) ) );

R:=VWAP+((STD*DEV3));

Deviation 2 Curve:

day:= BarsSince(BarIx(@,StartOf Day) = 0,1,10000)+1;

day2:= BarsSince(BarIx(@,StartOf Session) = 0,1,10000)+1;

priceX:= IF(price = 1, Close(@), IF(price = 2, High(@), IF(price = 3, Low(@), IF(price = 4, Mid(@), IF(price = 5, HLC3(@), IF(price = 6, Avg(@), IF(price=7, Open(@), 0) ) ) ) ) ) ) ;

vol:= IF( HasVal(Vol(@)) AND Vol(@) > 0, Vol(@), 1) ;

a:= Sum(priceX* vol,day)/ Sum(vol,day);

b:= Sum(priceX* vol,day2)/ Sum(vol,day2);

c1:= Sum(priceX* vol,Period)/ Sum(vol,Period);

VWAP:= IF(DaySessionPeriod = 1, a, IF(DaySessionPeriod = 2, b, IF(DaySessionPeriod = 0, c1, a) ) );

DAYSES:= STDDEV(@,day)/100;

SES:= STDDEV(@,day2)/100;

ANY:= STDDEV(@,Period);

STD:=IF(DaySessionPeriod = 1, DAYSES, IF(DaySessionPeriod = 2, SES, IF(DaySessionPeriod = 0, ANY, ANY) ) );

VWAP+((STD*DEV2));

Deviation 1 Curve:

day:= BarsSince(BarIx(@,StartOf Day) = 0,1,10000)+1;

day2:= BarsSince(BarIx(@,StartOf Session) = 0,1,10000)+1;

priceX:= IF(price = 1, Close(@), IF(price = 2, High(@), IF(price = 3, Low(@), IF(price = 4, Mid(@), IF(price = 5, HLC3(@), IF(price = 6, Avg(@), IF(price=7, Open(@), 0) ) ) ) ) ) ) ;

vol:= IF( HasVal(Vol(@)) AND Vol(@) > 0, Vol(@), 1) ;

a:= Sum(priceX* vol,day)/ Sum(vol,day);

b:= Sum(priceX* vol,day2)/ Sum(vol,day2);

c1:= Sum(priceX* vol,Period)/ Sum(vol,Period);

VWAP:= IF(DaySessionPeriod = 1, a, IF(DaySessionPeriod = 2, b, IF(DaySessionPeriod = 0, c1, a) ) );

DAYSES:= STDDEV(@,day)/100;

SES:= STDDEV(@,day2)/100;

ANY:= STDDEV(@,Period);

STD:=IF(DaySessionPeriod = 1, DAYSES, IF(DaySessionPeriod = 2, SES, IF(DaySessionPeriod = 0, ANY, ANY) ) );

VWAP+((STD*DEV1));

Vwap:

day:= BarsSince(BarIx(@,StartOf Day) = 0,1,10000)+1;

day2:= BarsSince(BarIx(@,StartOf Session) = 0,1,10000)+1;

priceX:= IF(price = 1, Close(@), IF(price = 2, High(@), IF(price = 3, Low(@), IF(price = 4, Mid(@), IF(price = 5, HLC3(@), IF(price = 6, Avg(@), IF(price=7, Open(@), 0) ) ) ) ) ) ) ;

vol:= IF( HasVal(Vol(@)) AND Vol(@) > 0, Vol(@), 1) ;

a:= Sum(priceX* vol,day)/ Sum(vol,day);

b:= Sum(priceX* vol,day2)/ Sum(vol,day2);

c1:= Sum(priceX* vol,Period)/ Sum(vol,Period);

VWAP:= IF(DaySessionPeriod = 1, a, IF(DaySessionPeriod = 2, b, IF(DaySessionPeriod = 0, c1, a) ) );

DAYSES:= STDDEV(@,day)/100;

SES:= STDDEV(@,day2)/100;

ANY:= STDDEV(@,Period);

STD:=IF(DaySessionPeriod = 1, DAYSES, IF(DaySessionPeriod = 2, SES, IF(DaySessionPeriod = 0, ANY, ANY) ) );

VWAP

- Deviation 1:

day:= BarsSince(BarIx(@,StartOf Day) = 0,1,10000)+1;

day2:= BarsSince(BarIx(@,StartOf Session) = 0,1,10000)+1;

priceX:= IF(price = 1, Close(@), IF(price = 2, High(@), IF(price = 3, Low(@), IF(price = 4, Mid(@), IF(price = 5, HLC3(@), IF(price = 6, Avg(@), IF(price=7, Open(@), 0) ) ) ) ) ) ) ;

vol:= IF( HasVal(Vol(@)) AND Vol(@) > 0, Vol(@), 1) ;

a:= Sum(priceX* vol,day)/ Sum(vol,day);

b:= Sum(priceX* vol,day2)/ Sum(vol,day2);

c1:= Sum(priceX* vol,Period)/ Sum(vol,Period);

VWAP:= IF(DaySessionPeriod = 1, a, IF(DaySessionPeriod = 2, b, IF(DaySessionPeriod = 0, c1, a) ) );

DAYSES:= STDDEV(@,day)/100;

SES:= STDDEV(@,day2)/100;

ANY:= STDDEV(@,Period);

STD:=IF(DaySessionPeriod = 1, DAYSES, IF(DaySessionPeriod = 2, SES, IF(DaySessionPeriod = 0, ANY, ANY) ) );

VWAP - ((STD*DEV1));

-Deviation 2:

day:= BarsSince(BarIx(@,StartOf Day) = 0,1,10000)+1;

day2:= BarsSince(BarIx(@,StartOf Session) = 0,1,10000)+1;

priceX:= IF(price = 1, Close(@), IF(price = 2, High(@), IF(price = 3, Low(@), IF(price = 4, Mid(@), IF(price = 5, HLC3(@), IF(price = 6, Avg(@), IF(price=7, Open(@), 0) ) ) ) ) ) ) ;

vol:= IF( HasVal(Vol(@)) AND Vol(@) > 0, Vol(@), 1) ;

a:= Sum(priceX* vol,day)/ Sum(vol,day);

b:= Sum(priceX* vol,day2)/ Sum(vol,day2);

c1:= Sum(priceX* vol,Period)/ Sum(vol,Period);

VWAP:= IF(DaySessionPeriod = 1, a, IF(DaySessionPeriod = 2, b, IF(DaySessionPeriod = 0, c1, a) ) );

DAYSES:= STDDEV(@,day)/100;

SES:= STDDEV(@,day2)/100;

ANY:= STDDEV(@,Period);

STD:=IF(DaySessionPeriod = 1, DAYSES, IF(DaySessionPeriod = 2, SES, IF(DaySessionPeriod = 0, ANY, ANY) ) );

VWAP - ((STD*DEV2));

-Deviation 3:

day:= BarsSince(BarIx(@,StartOf Day) = 0,1,10000)+1;

day2:= BarsSince(BarIx(@,StartOf Session) = 0,1,10000)+1;

priceX:= IF(price = 1, Close(@), IF(price = 2, High(@), IF(price = 3, Low(@), IF(price = 4, Mid(@), IF(price = 5, HLC3(@), IF(price = 6, Avg(@), IF(price=7, Open(@), 0) ) ) ) ) ) ) ;

vol:= IF( HasVal(Vol(@)) AND Vol(@) > 0, Vol(@), 1) ;

a:= Sum(priceX* vol,day)/ Sum(vol,day);

b:= Sum(priceX* vol,day2)/ Sum(vol,day2);

c1:= Sum(priceX* vol,Period)/ Sum(vol,Period);

VWAP:= IF(DaySessionPeriod = 1, a, IF(DaySessionPeriod = 2, b, IF(DaySessionPeriod = 0, c1, a) ) );

DAYSES:= STDDEV(@,day)/100;

SES:= STDDEV(@,day2)/100;

ANY:= STDDEV(@,Period);

STD:=IF(DaySessionPeriod = 1, DAYSES, IF(DaySessionPeriod = 2, SES, IF(DaySessionPeriod = 0, ANY, ANY) ) );

VWAP - ((STD*DEV3));

-

Can someone, or Dbtina, pls pls help me check if anything needs to be modified? I had the code below sent and i am using cqg

day:= BarsSince(BarIx(@,StartOf Day) = 0,1,10000)+1;

day2:= BarsSince(BarIx(@,StartOf Session) = 0,1,10000)+1;

priceX:= IF(price = 1, Close(@), IF(price = 2, High(@), IF(price = 3, Low(@), IF(price = 4, Mid(@), IF(price = 5, HLC3(@), IF(price = 6, Avg(@), IF(price=7, Open(@), 0) ) ) ) ) ) ) ;

vol:= IF( HasVal(Vol(@)) AND Vol(@) > 0, Vol(@), 1) ;

a:= Sum(priceX* vol,day)/ Sum(vol,day);

b:= Sum(priceX* vol,day2)/ Sum(vol,day2);

c1:= Sum(priceX* vol,Period)/ Sum(vol,Period);

VWAP:= IF(DaySessionPeriod = 1, a, IF(DaySessionPeriod = 2, b, IF(DaySessionPeriod = 0, c1, a) ) );

DAYSES:= STDDEV(@,day)/100;

SES:= STDDEV(@,day2)/100;

ANY:= STDDEV(@,Period);

STD:=IF(DaySessionPeriod = 1, DAYSES, IF(DaySessionPeriod = 2, SES, IF(DaySessionPeriod = 0, ANY, ANY) ) );

R:=VWAP+((STD*DEV3));

-

wonder if anyone has a code or so for cqg for the vwap bands.....

Been having a hard time scripting them to even think about using

-

hmmm....

these are the coding they gave me though.... i will go back and see if there is any more.

But u guys seem to know it better though. Is the script above considered a "code" ?

-

damn..... i do not know coding at all... this is something that the cqg sent me.

sheesh.... wonder if anyone can help me

-

seems similiar........

u any idea if my coding is correct though?

-

Managed to upload a file, seems slightly different le.... I am in Asia timing so i am nt sure if its accurate, anyway posted e coding i made,

Could u roughly check plszzzzzzz ??

day:= BarsSince(BarIx(@,StartOfDay) = 0,1,10000)+1;

day2:= BarsSince(BarIx(@,StartOfSession) = 0,1,10000)+1;

priceX:= IF(price = 1, Close(@), IF(price = 2, High(@), IF(price = 3, Low(@), IF(price = 4, Mid(@), IF(price = 5, HLC3(@), IF(price = 6, Avg(@), IF(price=7, Open(@), 0) ) ) ) ) ) ) ;

vol:= IF( HasVal(Vol(@)) AND Vol(@) > 0, Vol(@), 1) ;

a:= Sum(priceX* vol,day)/ Sum(vol,day);

b:= Sum(priceX* vol,day2)/ Sum(vol,day2);

c1:= Sum(priceX* vol,Period)/ Sum(vol,Period);

VWAP:= IF(DaySessionPeriod = 1, a, IF(DaySessionPeriod = 2, b, IF(DaySessionPeriod = 0, c1, a) ) );

DAYSES:= STDDEV(@,day)/100;

SES:= STDDEV(@,day2)/100;

ANY:= STDDEV(@,Period);

STD:=IF(DaySessionPeriod = 1, DAYSES, IF(DaySessionPeriod = 2, SES, IF(DaySessionPeriod = 0, ANY, ANY) ) );

R:=VWAP+((STD*DEV3));

-

Does no1 has vwap for cqg?

arugh.....

was thinking i could customise some studies to imitate vwap, been racking my head for some time.

-

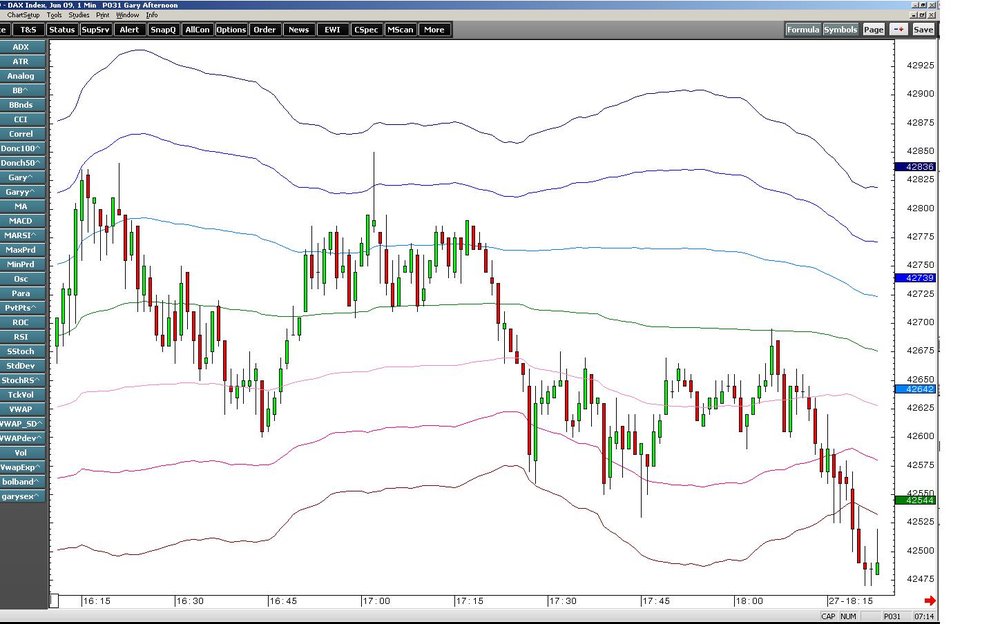

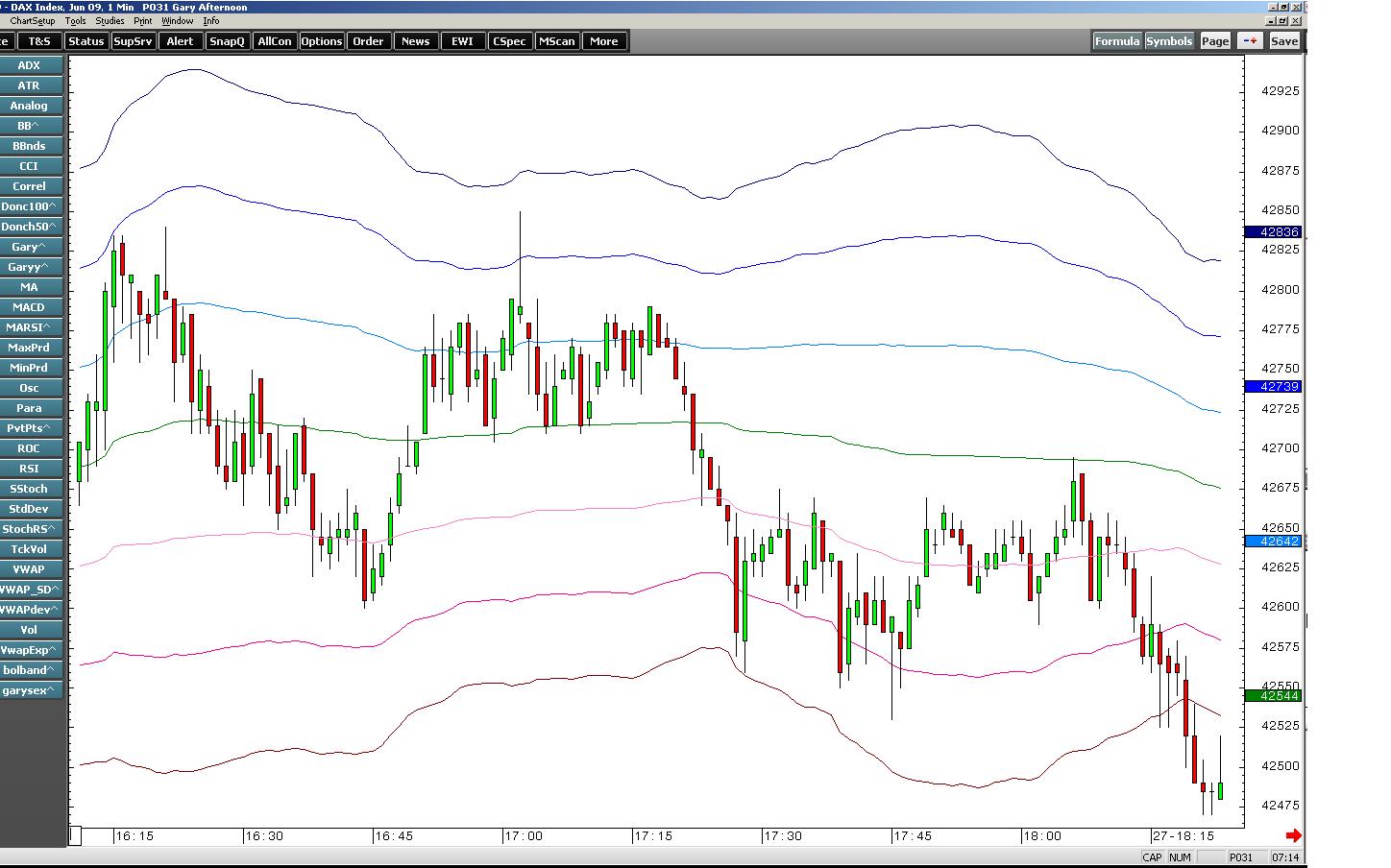

no no, by jerky i mean the bands stick to each bar in a very skewy way.

I shd attach a screenshot for u to see... arugh

The cqg person didnt really understand what i was trying to say...

sigh

-

seems like someone struggling like me with the bands lol

-

Does jerky bars correspond to ur charts?

-

hmmmmm a bit of dilemma, i use 1 period for 2 min charting is possible, but the charting turns out terribily jerky ...... but it seems to smooth out when i use longer periods of calcualtion for SD bands.....

-

Managed to do something abt the bands in cqg, however may i ask if the bands recalculation period i set to 28 periods for 2 min periods, would it be more accurate?

i noted that if i set it to recalculate per 2 min, my chart becomes very jerky and messy, and setting it to a longer period per recalculation makes it smoother.

Is it wrong?

BTW, i got a very impt question, 2 STD DEV is 2 X 1STD DEV right? just wanan clarify.

cos this means if i managed to calcualte 1 std dev, 2 or 3 std dev shld nt be a prob

-

Managed to do something abt the bands in cqg, however may i ask if the bands recalculation period i set to 28 periods for 2 min periods, would it be more accurate? i noted that if i set it to recalculate per 2 min, my chart becomes very jerky and messy, and setting it to a longer period per recalculation makes it smoother.

Is it wrong?

BTW, i got a very impt question, 2 STD DEV is 2 X 1STD DEV right? just wanan clarify.

cos this means if i managed to calcualte 1 std dev, 2 or 3 std dev shld nt be a prob

-

I found this post on "Re: Trading with Market Statistics XI. HUP" interesting and have nominated it accordingly for "Topic Of The Month March, 2009"

-

oh u mean soul trader....

-

whos James? Is that his TL nick

-

awww...... i been thinking n scratching my head again and again to come up with vwap bands...... was hoping someone can help me out

-

u mean bolligner bands???

those arent vwap sd bands right

-

yah, they seem to have vwap though but no sd bands. i am confused as to how to customise the bands as i know it is possible to do so

-

--------------------------------------------------------------------------------

I am confused as i am using CqG and i am not sure how i should go about creating customised SD bands.

Is anyone using CQG ?

Please kindly help.

Many thanks....

-

I am confused as i am using CqG and i am not sure how i should go about creating customised SD bands.

Is anyone using CQG ?

Please kindly help.

Many thanks....

ProfLogic's Method

in Swing Trading and Position Trading

Posted

cqg begining to suck